The Client Story

A risk and regulation advisory practice serving banks across the MENA region. The practice was preparing the next round of conversations with bank credit teams — and slide decks were no longer enough. Bank stakeholders wanted a tool that the advisor could open in the room, run on a real anonymized statement, and discuss against their own portfolio.

The brief was narrow and time-bound: a working artefact for live senior-credit demos, not a six-month implementation roadmap. That brief is exactly the shape of an AI prototyping engagement — a defensible, demo-safe artefact that earns the right to the next conversation.

| Service: | AI Prototyping |

|---|---|

| Industry: | Financial Services |

| Year: | 2026 |

| Location: | MENA |

Read summarized version with

"We invest a week or so, wherein we talk about the couple of problem statements that we are facing with our clients in terms of the kind of analytics they want to do."

— Partner, FS Consulting

"The POC is only for the purpose to provide a demo to the client that look here — this is not only on paper."

— Senior Manager, FS Consulting

Why a Prototype, Not a Slide Deck

SME underwriting across MENA still runs on manual document review and bureau scoring. Banks hold rich transaction data — but have no pipeline to convert it into behavioral signals. Thin-file SMEs, the majority of the market, are rejected by default.

The advisory practice needed something a senior advisor could open in the room, drop a real anonymized statement into, and discuss against their own portfolio. A slide deck couldn’t do that. A working prototype could.

In regulated finance, slide-stage proposals stall at the legal/risk layer — stakeholders want to see signals on screen before they commit to scoping. GroupBWT’s AI prototyping is built for exactly that moment:

- Working artefact in weeks, not months. Built around a synthetic dataset with realistic behavioral patterns — demos run from day one without touching real customer data.

- Demo-safe by design. Presentable in regulated boardrooms with no real customer record on screen; the same codebase later moves inside the client’s perimeter for production.

- Two paths from one codebase. BRD handoff or foundation for a follow-on build — the choice is made after stakeholder conversations land.

- Defensible AI. Every signal traces back to a specific transaction or evidence record. No hallucinated scores in front of a credit committee.

The MENA SME credit demo below is one application of that approach.

The AI Prototyping Approach, Applied to SME Credit Scoring

GroupBWT delivered the prototype in two phases — the same structure used across our AI prototyping engagements.

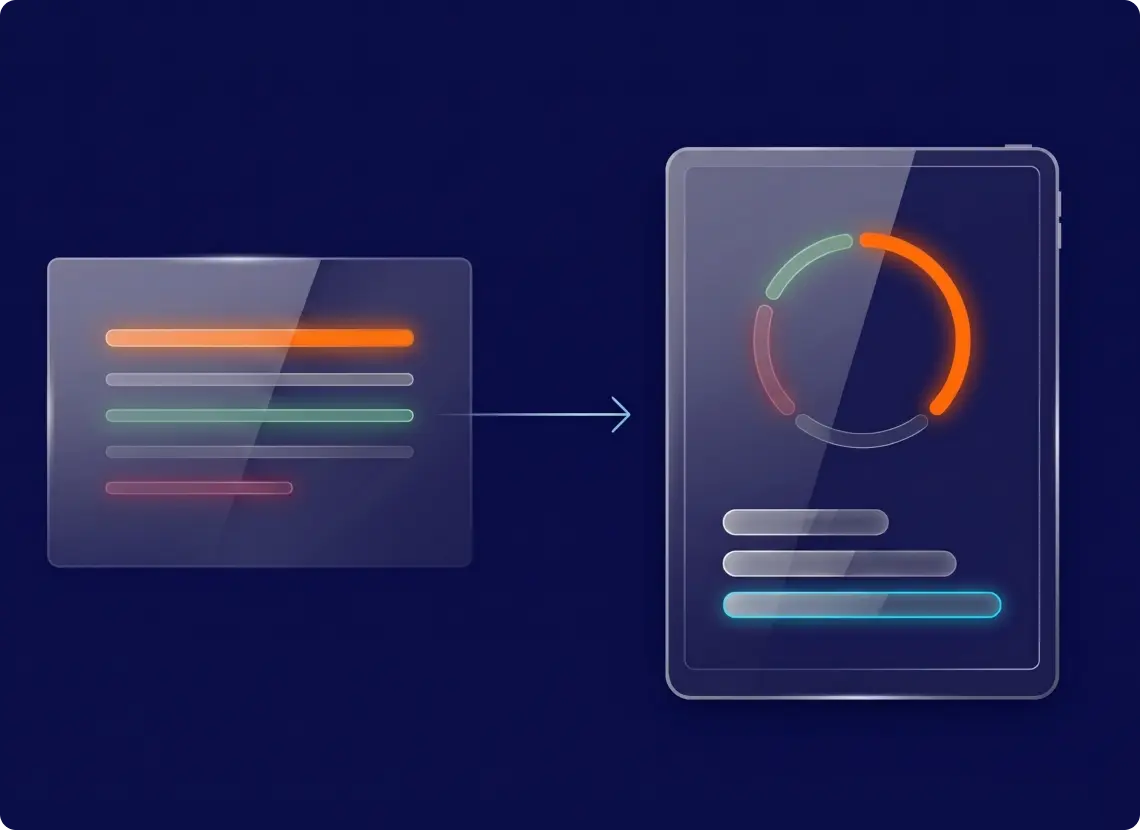

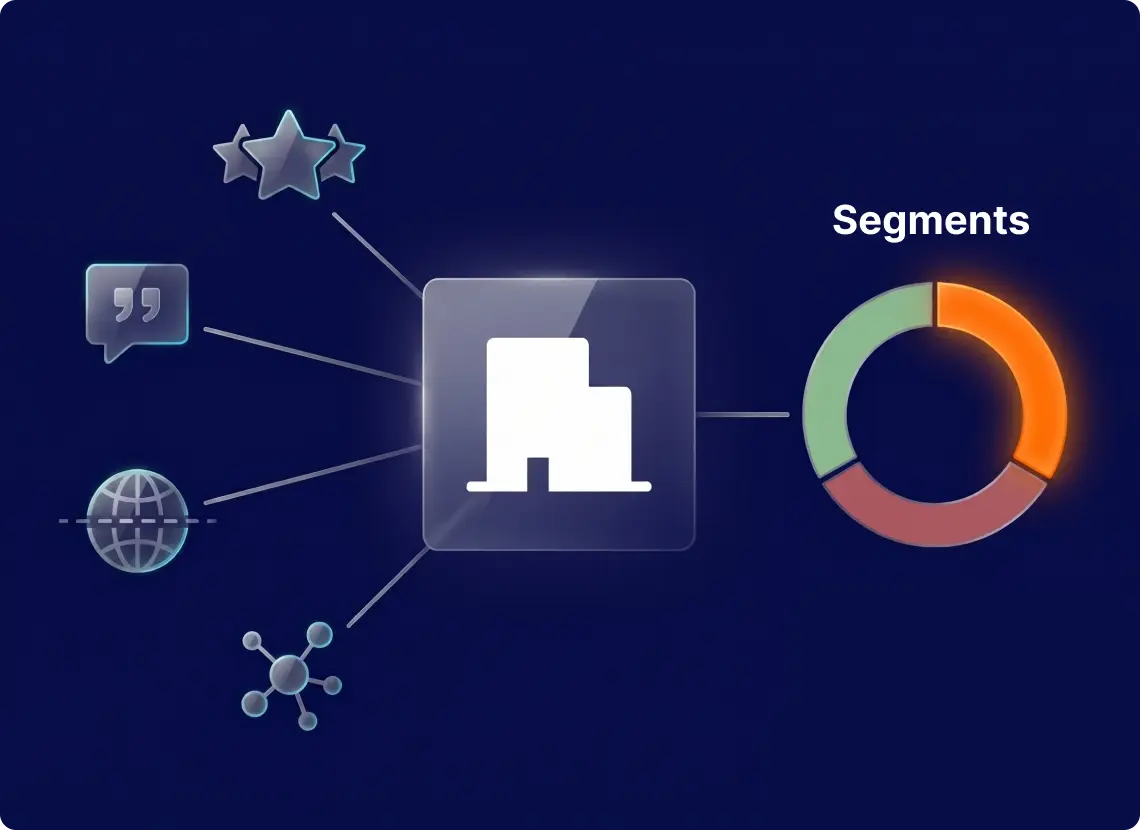

1. Phase one — Digital-footprint check (Maturity Checker). A credit officer enters an SME applicant; the prototype aggregates publicly available digital-footprint signals (review presence, domain history, social activity) via compliant collection methods. Output: a Red / Amber / Green readout across three sub-scores — legitimacy, continuity, reputation — with each score citing the specific evidence behind it. A defensible pre-screening view in a single working session.

On thin profiles, an LLM will just make things up — and 'made things up' is unshippable in regulated finance. The engineering work was making the AI accountable: every signal traceable to a specific transaction, every score citing its evidence.

2. Phase two — Live signal generation from bank statements

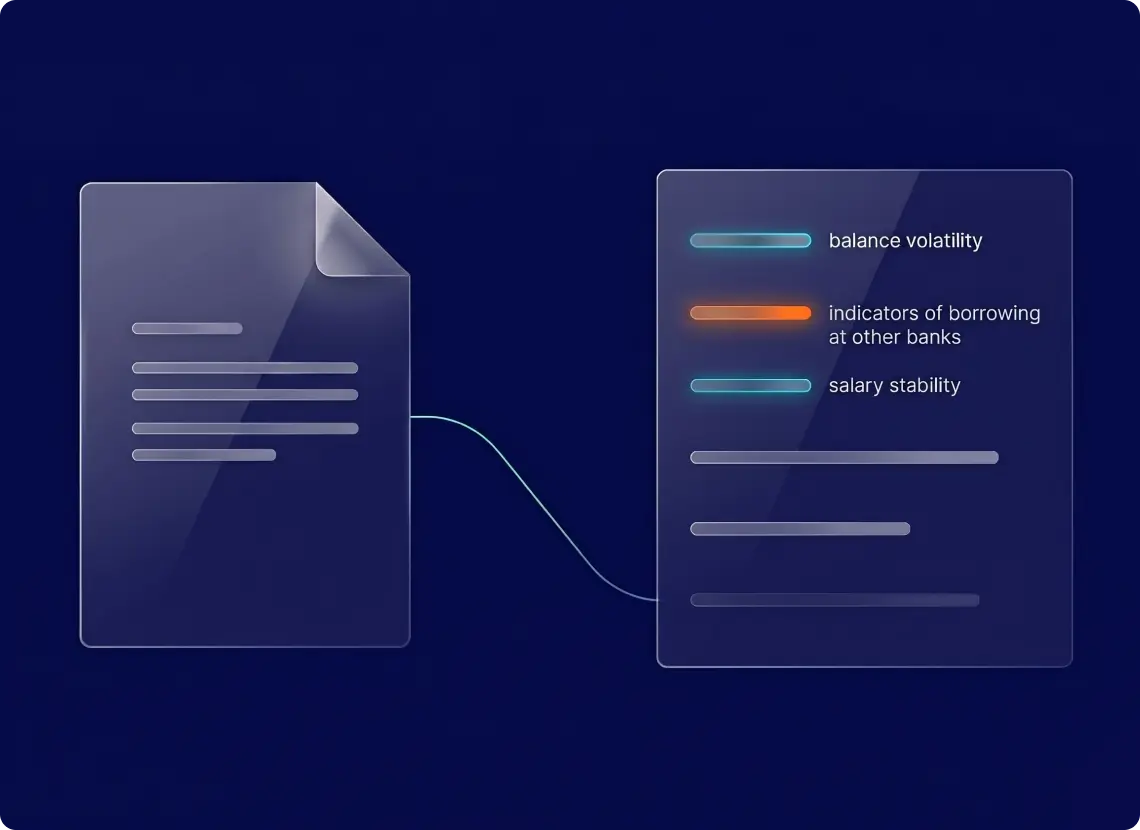

A credit officer drops an anonymized PDF statement into the prototype. The system extracts and classifies transactions (LLM-assisted), then a deterministic scoring layer surfaces 5–7 high-impact signals: balance volatility, indicators of borrowing activity at other banks, salary stability, debt-to-income ratio, expense compression, overdraft frequency, and remittance ratio. PDF intake keeps the prototype source-agnostic until regional Open Banking APIs go live.

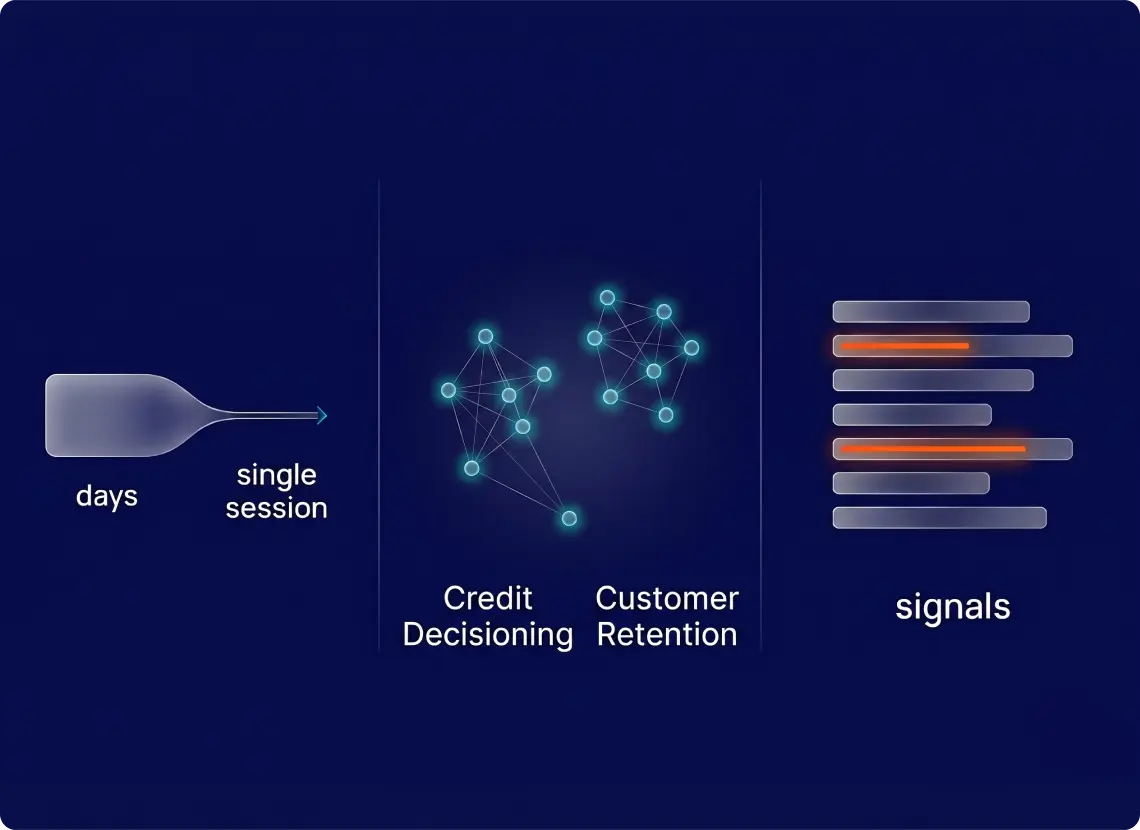

3. Sequenced use-case backlog (11 use cases). Mapped across credit decisioning (creditworthiness, balance transfer, cross-sell, multi-offer engine) and customer retention (salary outflow, remittance, cash sweep, life events, churn risk, dormant accounts, subscription optimization). Sequencing reflects which signals deliver value fastest.

The prototype runs on a small synthetic dataset — no real customer records on screen. Thresholds and weights read from configuration, so the same codebase tunes to each bank’s risk appetite without an engineering ticket. The engagement ends either as a BRD handoff or as the foundation for an in-bank build.

Tech stack: Python; AI-assisted public-web signal aggregation; LLM-assisted transaction classification + deterministic heuristic scoring with mandatory citation grounding; PDF statement intake; configuration-driven thresholds and weights; synthetic dataset for demo-safe runs.

What the Prototype Is Designed to Enable

- Pre-screening that historically takes days collapses into a single working session.

- Every signal on screen cites its evidence — defensible in front of a credit committee.

- A sequenced backlog of 11 use cases across credit decisioning and retention, ready for a phased bank rollout.

Need an AI Prototype Your Senior Stakeholders Can Click Through?

For teams that need a defensible AI prototype — runnable on real anonymized data, safe in regulated boardrooms, configurable to each institution's appetite, and ready to graduate from BRD into a production build when the conversation lands.

You have an idea?

We handle all the rest.

How can we help you?